True Money Supply

Having discussed the status-quo money supply measures M0, MB, M1, & M2; as well as brief descriptions of their constituent inputs, we turn our attention the Austrian Rothbard-Salerno true money supply measure (TMS).

It should come as no surprise that the Misesian Austrian economists disagree with the mainstream clown economists on what constitutes the money supply, which in turn defines inflation for the Austrian school. Elaborated here is the Rothbard-Salerno TMS measure. A full discussion/analysis on the definition of money and “moneyness” shall be delayed for a more focused treatment.

I have as of yet been unable to find explicit definitions for the following other measures using actively-available Federal Reserve input data, despite these being discussed in Austrian economic articles. The Fed’s definition of the money supply has changed over time (e.g. traveler’s check tracking stopping in 2018) and this makes it difficult to reformulate from current data Austrian definitions that were formulated a number of years ago. The additional measures are mentioned to emphasize simply that other Austrian measures exist, and there is disagreement among Austrian economists as to what should be considered components of the true money supply.

- AMS: Shostak’s Austrian Money Supply

- TMS1: “narrow” Austrian money supply - similar to AMS (if not the same)

- TMS2: “broad” Austrian money supply - similar to Rothbard/Salerno’s TMS (if not the same)

I am constructing TMS the following way, using the method described in Griggs & Murphy’s 2021 paper:

- M2 - starting point

- subtract the following

- small time deposits

- retail money funds

- add the following:

- US Treasury general account

- international deposits at the fed

Mises.org uses the Rothbard-Salerno metric and seems to employ the same construction, though might exclude the international deposits at the fed. Their definition in this article and is as follows: “This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits and retail money funds).”

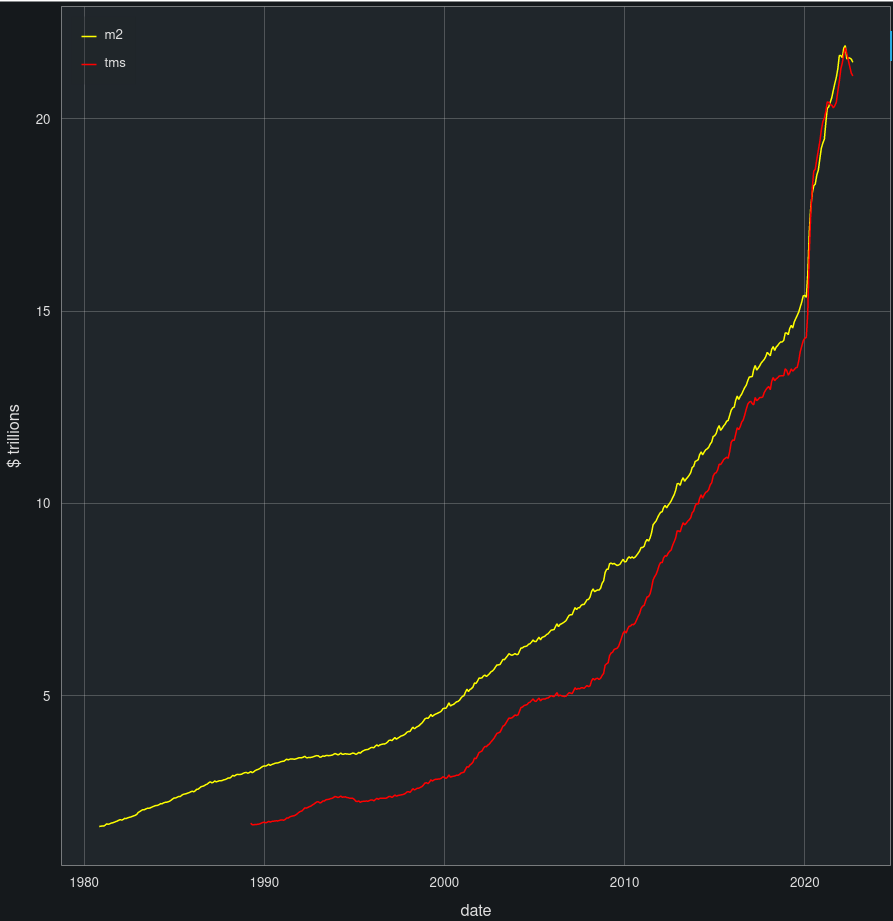

Using the Griggs & Murphy definition, which specifies use of monthly non-seasonally adjusted data, I have automated pulling the constituent components and graphing M2 against TMS, as well as their year over year percentage values (yoy %) - see plots below. These are posted now on https://www.truemoneysupply.com. Note: these are not, as of yet, automatically updated.

Prior to a more thorough treatment of “moneyness,” a few points should be made on money supply components. First, they are dynamic, changing as subjective consideration of them change (subjective theory of value applies to money) as well as the components themselves might change (e.g. regulatory changes might convert something from money into a loan/not-money). Secondly, they often include “fuzzy” elements where even Austrians cannot achieve clear consensus on whether a component is ostensibly money or not. Savings accounts are one example of this. Shostak et al. do not consider them on-demand because of the legal possible 30-day delay in cashing them out, vs. Rothbard et al. consider savings accounts money because the delay is not enforced. Time-deposits are another example: while not included in the Rothbard-Salerno measure, Rothbard at least at point argued that the ability to cash them out early on-demand for a penalty (i.e. below-par) implied that they should be included in money supply at the fixed penalty rate.

So with the elaboration of at least one Austrian metric for money supply, beyond the exclusive metrics of clown world economists working at the Fed, we shall at a later date elaborate more the concept of “moneyness.”